Coined by MIT Researcher Alan Thorogood, the phrase ‘hug of dying’ refers to a state of affairs the place the mismatch between the financial institution’s and fintech’s priorities and their relative speeds leads to the fintech’s sources being over listed and a failure to realize the fintech’s strategic targets.

Fintechs thrive once they transfer quick and thru “constant progress in prospects, funds and transactions, which in flip facilitates capital elevating and scaling of their merchandise and companies,” says Scott Simari, Principal of Sendero Consulting.

Banks nevertheless transfer slowly as a result of they’ve to take care of compliance, handle danger and stop product cannibalization, mentioned Simari.

“It’s the infinite committees, conferences, tollgates and critiques – typically lots of exercise and pressure on the fintech’s sources with out significant productiveness. From the fintech’s perspective, it’s a chance value drawback; the time and sources spent on supporting the monetary establishment could possibly be higher utilized to realize their very own strategic targets,” he mentioned.

There’s a lot to be mentioned in regards to the boons of bank-fintech partnerships and the way they’ll push the monetary business in the direction of innovation. There’s a lot that may go unsuitable, too.

A lot discuss, no cash

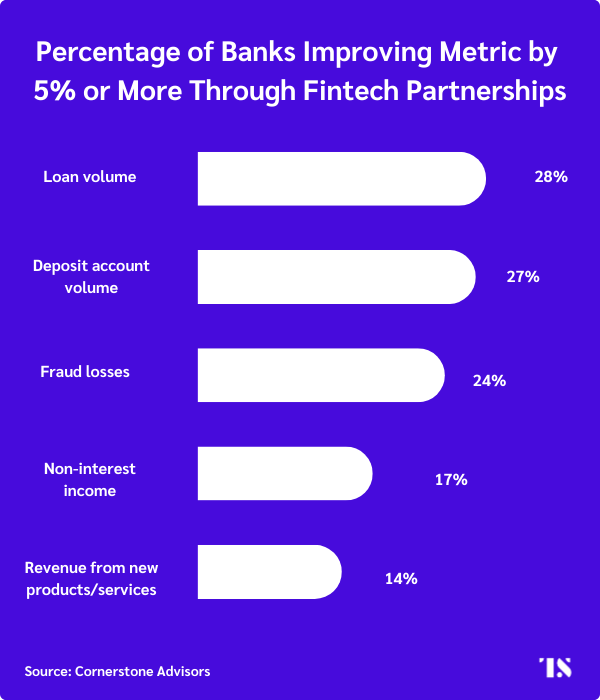

For banks, one of many worst issues that may occur with partnerships is investing right into a relationship with a fintech firm that bears little fruit. For instance, mortgage productiveness and mortgage quantity are main priorities for banks to hunt a partnership with fintechs, however solely 28% of banks report seeing 5% or extra enchancment in these areas, in keeping with research.

Partnering successfully is troublesome: Banks have to spend so much of time vetting potential companions after which integrating their tech of their core and ancillary techniques. Past the technical points, the paperwork inside banks may delay market occasions.

This barge-like motion might imply delayed or diminished outcomes for the financial institution, however for the fintech it may be akin to a dying sentence.

The partnership processes to be careful for

1) The compliance labyrinth: For banks compliance is a little bit cherished however crucial a part of their operations, which implies a fintech can discover a lot of its time being spent on making certain they meet the requirements and conversely, much less time spent on actions that may assist the fintech develop. “Capital elevating is intense; eighty % of my time is spent on it,” a fintech founder instructed Thorogood throughout his analysis.

2) The regulatory rigmarole: “The big establishment’s rigorous regulatory necessities and danger administration protocols can disproportionately eat the fintech’s sources, leaving them with restricted bandwidth to innovate and iterate on their platform,” mentioned Simari.

Not solely do these processes take away time from capital elevating talents, additionally they go away fintechs with restricted sources to spend on the betterment of their very own providing. This stagnation will be harmful particularly if the fintech is partnering with a really large and properly acknowledged financial institution. “A fintech can danger its id being overshadowed by the monetary establishment, leading to a lack of autonomy and strategic route,” he mentioned.

Easy methods to keep away from the hug of dying

The hug of dying isn’t good for both accomplice. Whereas the financial institution might profit initially from the fintech dedicating a big chunk of its sources to the connection, the stagnation that the fintech might expertise on account of this, impacts what advantages a financial institution can reap down the road. Avoidance of an over-exerting partnership like that is the very best coverage:

- Launch independently first: Companions can think about standalone launches quite than diving headfirst and integrating merchandise with enterprise platforms. “This strategy facilitates swift market entry, allows simple analysis of worth and permits for simple separation if crucial,” mentioned Simari.

- Preserve your scopes in verify: The hug of dying is extra prone to happen if the partnership’s scope will increase in a short time, which ends up in “dependency on numerous enterprise capabilities,” he mentioned. The increasing remit of the partnership may cause delays and inside conflicts, in addition to extra prices for the FI. So partnerships ought to begin small and with clear goals from day one.

- Set boundaries: Fintechs ought to clearly outline the connection, distinguishing whether or not they’re a strategic or transactional accomplice, in keeping with Simari. This permits each companions to start out the worth matching course of early within the deal and mitigates any danger of the connection changing into an excessive amount of to bear for any accomplice.

“Fintechs’ transparency about their present capabilities is important, avoiding the temptation to oversell future product developments,” mentioned Simari.