dednuel photos

Dave Inc.’s Background Story

Dave Inc. (NASDAQ:DAVE) is a fintech firm that was began in 2016 by Jason Wilk. The corporate launched the Dave App in 2017. The corporate raised enterprise cash in 2018-2021. The corporate went public in late 2021 by way of a merger with a SPAC, VPC Influence Acquisition Holdings III, that valued Dave at $4bn. Regardless of having a wholesome ~10-20% revenue margin for many of its life as a non-public firm, after going public, Dave ramped up advertising and marketing and buyer acquisition spending, which drove giant losses in 2022 and 2023, masking the robust unit economics of the enterprise. Administration began pulling its profitability levers in 2023, and the outcomes are starting to indicate up now. There’s a vital upside to earnings estimates as the corporate continues to drive worthwhile progress. Particularly, administration is testing a brand new subscription pricing of $4/consumer/month for all clients who use Dave’s core money advance product. By my estimates, this alteration alone has the potential to drive the corporate’s EPS to over $10/share in 2025 or 2026 versus consensus EPS of $2.10 in 2025. In my base case, with none change in subscription pricing, I estimate Dave will earn $3.11 of EPS, which continues to be 50% above the road. I estimate the inventory is price over $100/share within the subsequent 12-18 months because the market realizes Dave’s earnings energy and enterprise worth.

How the enterprise works

Dave’s core product is a money advance of $25 to $500, which is utilized by US customers to assist keep away from overdraft charges and make ends meet. The enterprise serves underserved customers who usually flip to expensive examine cashing or payday loans. There are three strategies that buyers can use to borrow from Dave: first, immediate on Dave card which is a 3% payment, plus Dave earns interchange on the transactions which averages about 2%. Secondly, direct to checking account with Visa direct, which is a 5% payment. Lastly, by way of ACH switch to a checking account, which is free. Dave doesn’t cost curiosity on its money advances – solely the preliminary switch payment for sooner pace, much like Venmo and CashApp’s income mannequin of charging for quick supply. Dave has 2.2m month-to-month energetic members that every common three transactions per quarter for a complete of 6.6m transactions per quarter. The typical origination measurement is $159 and the typical income per transaction is $9, a 5.7% take price. As well as, Dave earns cash on suggestions and subscriptions. The money advances are mechanically repaid from the patron’s checking account as quickly as their paycheck hits the account. Dave’s credit score losses are about 1.3% of originations due to the best way they prolong the additional money merchandise. Dave begins with a $25 advance. If that quantity is repaid just a few occasions, they are going to progressively improve it over time, as much as a max of $500. The typical length is barely 14 days, so the speed of the advances could be very excessive, permitting Dave to regulate its credit score mannequin in real-time.

Dave competes with firms like Chime, MoneyLion, and Brigit. Chime is anticipated to IPO in 2025 which can drive an extra understanding of the money advance enterprise and a further comparable firm. Chime final raised capital in 2021 at a $25bn valuation.

Dave is an early adopter of synthetic intelligence, utilizing it each in its credit score fashions to find out which customers get money advance provides and for the way a lot and in addition in its name facilities, resolving 90% of tickets with out touching an agent. These outcomes enable Dave to supply higher customer support and a cheaper price level than opponents.

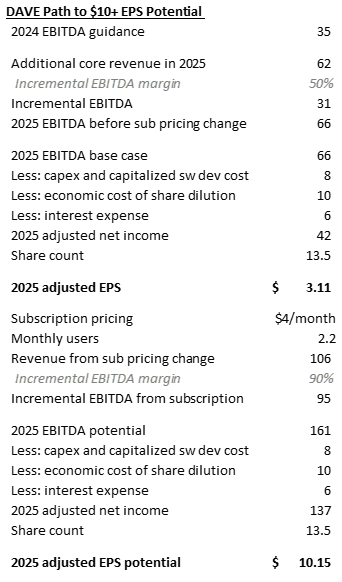

The trail to $10+ EPS

Up till the previous few months, Dave had no promote aspect analysts protection and few buyers understood Dave’s enterprise mannequin and potential. Consensus estimates haven’t caught as much as the extent of profitability that Dave is on observe to ship. I estimate in my base case, Dave will earn $3.11 of EPS. And has the potential to earn over $10 of EPS in 2025 or 2026 with the change in subscription pricing they’re testing and more likely to roll out later this yr.

As mentioned on the final earnings name, Dave applied a brand new billing system and is testing new subscription pricing. I estimate that Dave may implement $3-$5/month pricing for all of its month-to-month customers. At that worth level, it’s nonetheless a significant low cost to opponents resembling Brigit which cost over $10/month in subscription charges.

I estimate incremental 50% EBITDA margin on core enterprise progress, which is decrease than the 150% incremental margin DAVE has pushed during the last 5 quarters. The movement by way of of incremental income has been over 100% as a result of Dave has lowered the extent of spending on advertising and marketing and opex.

As well as, I estimate that Dave will generate $4/month on its 2.2m month-to-month energetic customers, driving an incremental $106m of income at 90% margin. This drives 2025 EBITDA potential to $161m, versus the road at $51m (the road just isn’t modeling subscription pricing change).

From there, eradicating capex and capitalized software program growth value, financial value of dilution, and curiosity expense ends in $137m of adjusted internet earnings. Divided by 13.5m diluted share depend, will get $10.15/share of adjusted EPS (financial earnings). The corporate is not going to pay taxes for a few years, given the big stability of NOLs. Be aware that stock-based compensation within the GAAP financials is predicated on inventory awards that have been granted on the time of the IPO at $320/share. I calculate financial dilution by trying on the market cap x share annual dilution from right here, which works out $400m x 2.5% = $10m/yr.

Firm steerage and my estimates

Valuation

In my base case, I estimate that Dave is price $3.11 x 16x P/E = $50/share. Nonetheless, if Dave executes on the subscription pricing change, I estimate that Dave is price effectively over $100/share primarily based on the $10.15 of EPS and no less than a 10x P/E. Dave presently trades at 14.2x, 2025 P/E. Making use of the identical earnings a number of to my estimate of 2025 EPS arrives at a worth of $144/share.

At $100, Dave could be valued at about $1.4bn which is meaningfully larger than its present valuation, however nonetheless considerably under the $4bn valuation that enterprise capitalists invested into the corporate in 2021 and the IPO valuation on the identical $4bn, regardless of Dave considerably rising income and inflecting the enterprise to software-like margins over 30%.

worth by way of a unique lens, shopper credit score firms spend lots of of {dollars} per consumer to amass new customers. Dave has 10.8m lifetime signups and a couple of.2m month-to-month energetic customers. At $150 per lifetime buyer signup, Dave is price $1.6bn, or $120/share. A strategic acquirer like Capital One or Citi could be excited by buying Dave and utilizing Dave’s knowledge on precise compensation historical past to make bank card provides to extremely engaged customers. Bank card merchandise are way more profitable than money advance. Over time, if Dave just isn’t acquired, the corporate could launch its personal bank card or credit score builder product.

Dangers

- Dave could not notice the earnings energy that I count on as a result of they won’t change the subscription pricing. Or customers could use Dave much less often if there’s a pricing change.

- Dave faces credit score danger. Whereas credit score metrics have meaningfully improved during the last a number of quarters, a weaker shopper may lead to larger delinquencies and better credit score losses.

- Potential regulatory change. Whereas Dave has by no means had any regulatory points, the CFPB or different regulators may additional regulate the money advance business, which might affect all the business, together with Dave.